Discrepancies in remittance and Cedi depreciation — The case of Ghana from 2016-2023

This study investigates the current practices for the compilation and dissemination of data on inward remittances discrepancies and its impact on the persistent depreciation Ghana’s Cedi over the past seven years.

As the structure of Ghana’s international trade remains as it is with the dominance of primary commodities in export and high imports, culminating in constant trade deficit, the local currency would continue to decline in value against the major trading currencies.

The failure on the part of Bank of Ghana to properly track, trace and capture all foreign remittances have contributed to persistent depreciation of local currency against the major trading currencies.

The Bank of Ghana’s 2023 annual report indicated that in 2023, 11 licensed FinTech companies provided inward remittance service to customers.

The total value of remittances received in 2023 was GH¢57 billion equivalent to US$ 5 billion, compared to GH¢18 billion equivalent to US$ 3billion in 2022.

The foreign exchange accumulated by these fintech companies are withholding close to US$ 8 billion accumulated from the foreign remittance space over the past two years and that have contributed to persistent depreciation of the local currency against the major trading currencies.

The rapid depreciation of the cedi against other major currencies destabilized the Ghanaian economy over the past decade and raised the economic consciousness of every Ghanaian regardless of his/her level of understanding of economic issues.

The effects of exchange rate depreciation are well documented in the literature. The one that frequently comes to mind is the fact that depreciation of real exchange rate increases demand for domestically produced goods by reducing their relative prices and more importantly promotes exports which eventually exert expansionary effect on national output.

This expenditure switching effects are associated with the Mundell-Fleming-Dornbusch framework. Thus, imports become more expensive relative to domestically produced goods particularly if domestic production does not depend largely on imported raw materials and capital inputs.

As the structure of Ghana’s international trade remains as it is with the dominance of primary commodities in export and high imports, culminating in constant trade deficit, the local currency would continue to decline in value against the major trading currencies.

The inflationary effect of the depreciation of the exchange rate is uncontestable particularly if, like Ghana, the country’s spending on imports constitutes a considerable proportion of total expenditure.

Cedi depreciation against major currencies does not only raise the cedi prices of final goods through imports of such goods but also through increased cedi costs of imported inputs.

Economic development experts and policymakers, in recent times, have developed keen interest in assessing the role of remittances in the economic development of Africa and other developing countries like Ghana.

Remittances are an addition not only to the domestic household income but also to the receipt side of the balance of payments.

Remittances offset chronic balance of payments deficits, by reducing the shortage of foreign exchange. This interest has arisen because remittances have emerged as an important source of development finance in developing countries since the 2000s.

In the face of dwindling official development assistance, poor inflows of foreign direct investments and inadequate private capital inflows, remittances are being relied upon by many developing countries to complement scarce domestic resources.

It is well-known that remittances, in whichever form, can enhance the socio-economic prospects of developing countries like Ghana. First, it is believed that remittance inflows can serve as a source of development finance through direct investment in the money and capital markets of beneficiary developing countries.

Secondly, remittances to developing countries can raise the level of technological development provided such remittances are used to finance income-generating value-added projects.

Thirdly, remittances may help improve consumer sovereignty by making the domestic markets more competitive through the provision of a wide array of goods and services.

Furthermore, it is believed that remittances, in a variety of ways can help promote exports, and hence improve upon the beneficiary country’s Balance of Payments (BoP) and international reserves.

The fact is that, in recent years, cross-border remittance flows have been on the rise with higher proportion of these flows going to developing countries.

The Ghanaian economy has also benefited from this increasing growth trend in remittance inflows. Remittances sent in foreign currencies typically required to be exchanged into domestic currency that is Ghana Cedi while foreign currencies in respect of foreign remittances translate higher foreign exchange reserves with Bank of

Ghana or with the 23 authorized dealer banks.

The World Bank global report (12/2023) showed that remittance flows to Sub-Saharan Africa increased by about 1.9% in 2023 to $54 billion, driven by strong remittance growth in Mozambique (48.5%), Rwanda (16.8%), and Ethiopia (16%).

Remittances to Nigeria, accounting for 38% of remittance flows to the region, grew by about 2%, while two other major recipients, Ghana and Kenya, posted estimated gains of 5.6% and 3.8%, respectively.

In Ghana for the period between 2020 to 2023 the licensing of new MTCs and 11 Fintech companies by Bank of Ghana have diverted the foreign exchange accruing from inward remittances to these institutions. In 2024, remittance flows to the region are projected to increase by 2.5%.

In Ghana, remittances have been increasing from its preceding period. It can prevent a balance of payment crises as well as having a positive impact on the economy.

In a micro sense, remittance plays an anti-poverty role due to increase in income, contributing to higher investment in education and healthcare remittance works as a means for investment.

In a broader sense, if the remittances are transferred through formal channels, it works as a source of foreign exchange reserve.

Remittances provide incentives to increase in consumption, demand for local goods or services, and job creation. Remittance stimulates aggregate demand and hence economic growth.

Remittance increases the reserve of the country, which is very important to feed up the Balance of payment (BoP). Remittance also affects price level in the presence of a weaker monetary control.

Inflows of remittances not only influence economic growth of recipient countries but also are a source to reduce current account deficits. Remittances are also considered a source to reduce internal and external borrowing of a country.

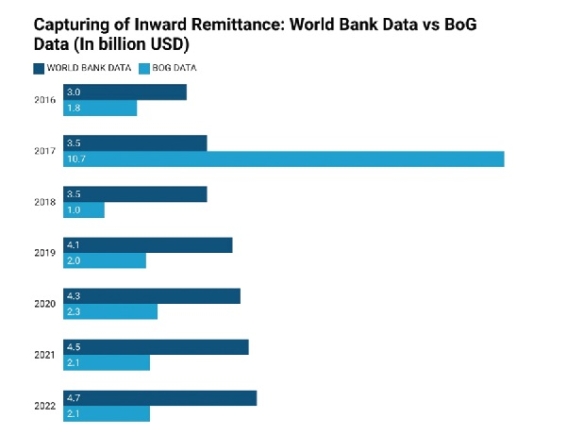

According to Bank of Ghana’s data on inward remittance, Ghana has witnessed a substantial rise in remittances inflow from US$1.8 billion in 2016, US$10.8 billion in 2017, US$1.1 billion in 2018, US$2.0 billion in 2019, US$2.3 billion in 2020, US$2.1 billion in 2021, US$ 2.1 billion in 2022, whilst the half year 2023 recorded US$1.3 billion.

However, according to World Bank data on inward remittance, Ghana has witnessed a substantial rise in remittances inflow from US$2 billion in 2014, US$5 billion in 2015, US$3 billion in 2016, US$3.5 billion in 2017 to US$4.5 billion in 2021 and further to US$4.7 billion in 2022; US$ 5.2 billion (World Bank 2023).

The above data analysis showed discrepancies between the World Bank data on inward remittances and actual remittances recorded by Bank of Ghana in the Consolidated Statement of Foreign Exchange Receipts and to enable the country to track and trace inward remittances could particularly be improved the country’s current account deficits as well as improving the stability of the local currency (Cedi).

This assertion has confirmed that Bank of Ghana has failed to track, trace, capture and strengthen the inflow of foreign remittances have not to stabilize the exchange rate, reducing the impact of currency fluctuations on the economy.

Government, Ministry of Finance and Bank of Ghana must address the weaknesses in the capturing of Inward Remittances Space.

It outlines discrepancies in this existing framework as well as the need for additional data from new MTOs and Fintech companies to address the anomalies identified in the World Bank data on inward remittances and that from Bank of Ghana’s data from the 23 authorized dealer commercial banks over the period 2016-2023.

The study also illustrates weaknesses in the country’s remittance data as against that of the assessment of World Bank’s remittance aggregates) and the need for specific practical guidance on data sources and compilation methods.

The inadequacy of practical compilation guidance concerns compilers, who, as a result, often produce data that is less credible than other balance of payments components.

As defined in the Balance of Payment Manual (BPM), the balance of payments (BOP) is a statistical statement that systematically summarizes, for a specific period, the economic transactions of an economy with the rest of the world.

Transactions, for the most part between residents and non-residents, consist of those involving goods, services, and income; those involving financial claims on, and liabilities to, the rest of the world; and those (such as gifts) classified as transfers, which involve offsetting entries to balance—in an accounting sense—one-sided transactions (International Monetary Fund, 1996).

Balance of payments statistics are included in a broad set of economic statistics known as the national accounts.

The System of National Accounts 1993 (1993 SNA) presents the conceptual framework for national accounts, and the fifth edition (1993) of the Balance of Payments Manual (the BPM) presents the conceptual framework and the structure and classification of the balance of payments.

The high level of concordance between the 1993 SNA and the BPM is extremely important. In Ghana, over the past decade, remittances have constituted an important component of balance of payments accounts, which is, usually, recorded as receipts under the capital account section by the Bank of Ghana. Ghana’s remittance receipts, in recent times, have assumed an increasing trend.

The micro- and macro-economic impact of remittances has been widely documented in the various World Bank country reports. At the macro level, remittances stabilize the balance of payments, hence contributing to closing the large and persistent trade gaps in many countries and preserving macroeconomic stability (World Bank, 2006).

At the micro-level, the development effects of remittances, with a certain degree of variety, have been documented for poverty alleviation, improving education and health outcomes, improving income distribution, and steering entrepreneurial spirit (Adams & Page, 2005).

Remittances are a rapidly growing and stable source of foreign exchange inflow to several developing economies like Ghana across the world.

Remittances through official sources far exceeded the size of official development assistance (ODA) and are more stable than foreign private flows such as portfolio investments like Euro-bond markets which are characterized by high volatility and distortionary tendencies due to their short life cycle.

Overview of money transfer companies and fintech companies in the inward remittance space in Ghana

Money transfer companies (MTCs) and financial institutions were the two central means of transferring and receiving cash in Ghana before 2019 where the Government passed the Payment Service and System Act 2019 Act 987 whereby new Money Transfer Companies and Fintech Companies into inward remittance space.

Through their global networks, these institutions have provided avenues for diaspora communities to remit money to Ghana.

They offered a variety of delivery service channels, such as direct-to-account, cash to the mobile phone, cash-to-card, and person-to-person transfers.

Their platforms are integrated to allow money transfers from bank to bank, from MTCs to bank, and through a mobile money system. According to World Bank data on inward remittance, Ghana has witnessed a substantial rise in remittances inflow from US$2 billion in 2014, US$5 billion in 2015, US$3 billion in 2016, US$3.5 billion in 2017 to US$4.5 billion in 2021 and further to US$4.7 billion in 2022; US$ 5.2 billion (World Bank 2023).

The Bank of Ghana’s estimates of the balance of payments suggested that remittances place second after exports in terms of resource inflow in Ghana.