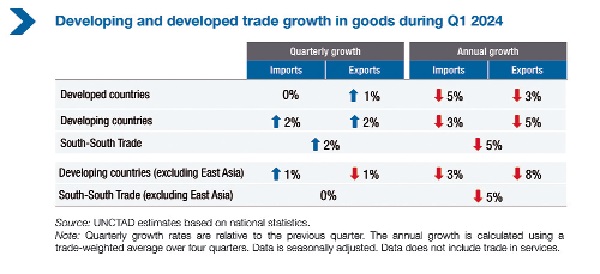

Global trade recovers, but unevenly (2)

Since the latter part of 2022, there has been a noticeable rise in the political proximity of trade. This indicates that bilateral trade patterns have been favouring trade between countries with similar geopolitical stances (i.e. friend-shoring). This trend stabilized from the second half of 2023.

Concurrently, there has been an increasing concentration of global trade to favour major trade relationships, although this trend also began to soften.

Geoeconomic issues continue to play a significant role in shaping key bilateral trade trends. These factors not only impact trade between the major economies but can also influence their trade dynamics with other trading partners.

Another significant factor impacting bilateral trade is the ongoing reshaping of value chains.

Global trade trends at the sectoral level

On a quarterly basis, most sectors experienced a rebound in Q1 2024. Most notable exceptions were transport and communication equipment, where trade contracted.

In contrast, quarterly increases were more pronounced for chemicals, pharmaceuticals, textiles, metals and minerals.

On an annual basis, global trade remains negative for many sectors, except for machinery, precision instruments, pharmaceuticals, transportation equipment, and road vehicles, the latter experiencing a strong increase in the trade of electric cars, which continued to rise even in Q1 2024, by about 25 per cent.

The value of trade in the last four quarters was still significantly lower for the energy and apparel sectors. Notably, trade in the communication and office equipment sectors continued to slide during Q1 2024.

Special Insight: Industrial policy and global trade

What is the issue?

Heightened geopolitical risks, the need for energy transition toward renewable sources, and significant technological advancements in computing power and artificial intelligence (AI) have led to an increase in government interventions in the economy.

Many of the interventions in developed and emerging markets have focused on support measures aimed at enhancing the competitiveness of strategic industries, positioning domestic firms as key suppliers of low-carbon products, and bolstering the resilience of supply chains for critical and strategic products.

Policies such as the United States Inflation Reduction Act, the Made in China 2025 initiative, and the European Union’s Net Zero Industry Act are largely motivated by strategic considerations related to the rapidly evolving environmental, technological, and geopolitical landscape.

How this relates to global trade?

The policy interventions currently implemented or considered by many governments take the form of industrial policy.

From a trade perspective, industrial policy typically seeks import substitution by providing support to domestic producers, imposing restrictions on trade, and facilitating vertical consolidations.

These types of interventions typically have a negative effect on trade.

One particularity of the policies being currently implemented is that, besides targeting well-established sectors like steel and aluminum where lobbying for support has historically been active, they are also forward-looking, focusing on sectors expected to experience a rapid increase in demand, both domestically and globally.

Government support in several major economies is now actively targeting industries associated with advanced technologies (such as high-end semiconductors) and renewable energies (such as electric batteries, electric vehicles, and solar panels).

Despite the generalized trade downturn, global demand in many of the sectors targeted by industrial policy has increased during 2023.

For instance, detailed product level data from the three major economies suggests that the trade in electric vehicles experienced a remarkable 50 per cent rise.

During the last few years global supply concentration, as measured by the Herfindahl–Hirschman index, has increased in most of the sectors targeted by industrial policy, but to varying degrees.

For instance, between 2022 and 2023, supply concentration rose significantly for batteries and their precursors, whereas it increased to a lesser extent in other sectors targeted by the industrial policies of major economies.

There has also been a varying degree of change in trade reallocation, indicated by the percentage of global supply shifting across countries, as measured by changes in global market shares.

Generally, higher trade reallocation rates indicate a more competitive market landscape where suppliers are vying for gains in market share. For example, product level data for three major economies indicates that about 12 per cent of the global supply of solar panels shifted between 2022 and 2023.

Importantly, while global competition appeared to have remained robust for solar panels and electric vehicles, this is not the case for battery value chains.

In this sector, the increase in supply concentration has been accompanied by low trade reallocation, suggesting that global supply is becoming increasingly concentrated in the hands of a few major exporters.

What are the possible implications for global trade?

Increased supply concentration. Industrial policy is likely to increase the concentration of the global supply of strategic products in even fewer economies.

By providing heavy subsidies to their own industries, developed countries and major emerging economies are expected to enhance their global competitiveness in these sectors.

This will impact not only their domestic markets but also global trade, potentially marginalizing smaller economies from entering these lucrative markets.

This may have important implications for developing countries.

Global trade fragmentation among major blocs. A subsidy race could lead to trade fragmentation among major suppliers seeking to gain trade dominance within their major trade relationships.

This will further affect the configuration of global value chains and global market segmentations, including upstream and downstream sectors.

Such an outcome would also increase tensions with the multilateral trading system, as many rules embedded in multilateral and bilateral or regional preferential trade arrangements limit countries’ ability to implement discriminatory trade policies or subsidy schemes with significant effects on trade.

Increased protectionism, trade costs, and uncertainty

Unilateral actions in the form of industrial policies often distort trade. Consequently, trading partners may respond with trade restrictions, escalating protectionism and potentially triggering retaliatory actions that undermine the rule- based global trading system.

Weaker international trade rules increase uncertainty in cross-border transactions, add complexity to business strategies, make it challenging to forecast costs and prices, and ultimately raise the costs of expanding into new markets for many firms, especially small and medium enterprises.