Honourable Minister,

It was empirically evidenced by all and sundry that Ghana’s economy made notable recovery strides in 2025, fueled by disciplined fiscal consolidation, effective monetary policy, and a rebound in key sectors such as services, agriculture, and exports.

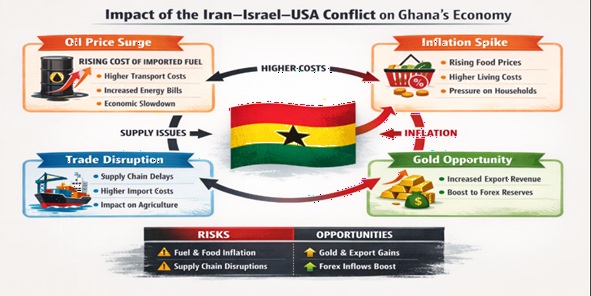

After years of macroeconomic instability, the country achieved strong quarterly growth, including a 5.5 per cent expansion in the third quarter of 2025, while consumer prices fell sharply from the triple-digit levels seen just a few years earlier. Inflation, which had peaked at over 50 per cent in 2022, declined dramatically, with headline inflation reaching single digits by late 2025, following years of concerted monetary tightening. These developments translated into tangible improvements: inflation control strengthened, investor confidence grew, and the cedi gradually stabilised, signalling a return to macroeconomic normalcy. However, the heightened geopolitical tensions involving Iran, Israel, and the United States introduce a new layer of uncertainty. These conflicts have already sent ripples through global energy markets, disrupted commodity supply chains, and created volatility in investor sentiment, risks that could easily spill over into Ghana’s fragile recovery if left unmitigated.

In this context, the nation’s economic resilience depends not only on sound domestic policies but also on its ability to navigate external shocks from distant conflicts, particularly those affecting trade, energy, and capital flows. A case in point is the Strait of Hormuz, a strategic waterway responsible for nearly 20% of global oil trade. Disruptions in this region immediately push up crude prices, which translate into higher fuel costs worldwide. For Ghana, which imports the majority of its refined petroleum, this means increased transportation costs, higher electricity tariffs, and renewed inflationary pressures, all of which can dampen domestic consumption and slow economic growth.

Even though Ghana is not an oil-exporting nation, the ripple effects of global energy shocks can strain government finances and weaken economic momentum. Analysts warn that the country’s heavy reliance on imports makes it particularly vulnerable to prolonged increases in oil and freight prices. In response, strategic policy measures, such as diversifying energy sources, enhancing fuel efficiency, and strengthening fiscal buffers, will be critical to safeguard Ghana’s economic gains and ensure resilience against global shocks.

Hon. Minister, understanding the multi-sector impact of current global developments requires linking international price movements and financial risk dynamics to Ghana’s domestic economic structures. I respectfully present an analysis of how key economic sectors are exposed to this conflict-induced shocks, integrating both global and domestic price data with the likely transmission mechanisms. This analysis highlights the channels through which external volatility can affect local production, investment, public finances, and overall economic stability, offering a clear foundation for informed and targeted policy responses.

Inflation and cost of living

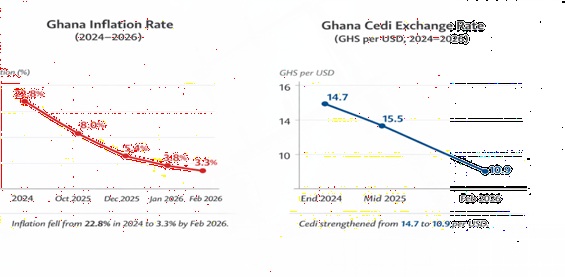

Over the years, it has become evident that much of Ghana’s inflation is not generated domestically but imported through rising global energy prices and exchange rate movements. In 2025, the country made impressive progress in controlling inflation, with headline rates falling to about 8 per cent by October and declining further to 3.8 per cent in January 2026, compared with the double-digit levels recorded in previous years. These improvements signalled easing price pressures and growing macroeconomic stability. However, the gains remain vulnerable to global shocks. When crude oil prices stay above $90 per barrel, fuel and transport costs rise, pushing up the prices of food and other essential goods. Even small increases in transport fares can make daily life more expensive for households, especially since food distribution and production depend heavily on fuel.

Exchange rate movements add another layer of pressure. Although improved foreign reserves helped reduce volatility in 2025, a weaker cedi still makes imports more expensive, and these costs are passed on to consumers in the form of higher prices for groceries and household goods. In response, the Bank of Ghana reduced its policy rate several times between 2025 and early 2026 to support economic recovery while maintaining price stability. Despite these efforts, imported price shocks, currency pressures, and high global energy costs continue to raise the cost of living. This gradually erodes purchasing power, with low-income households suffering the most because much of their income goes toward basic necessities.

Banking and financial services: Risk and capital flows

Financial markets are very sensitive to global events, especially geopolitical risks. When uncertainty rises worldwide, investors often pull back from emerging markets like Ghana, causing money to leave the country, putting pressure on the Cedi, and pushing up government and corporate borrowing costs. A clear example occurred in January 2026, when a spike in crude oil prices caused Ghana’s 5-year government bond yield to jump 40–60 basis points, reflecting investors’ worries about risk. These shifts make banks more cautious: they tighten lending, raise interest rates on loans, and limit long-term investment financing, which slows private sector growth.

Ghana has, however, made significant progress in recent years. After inflation soared above 50 per cent in early 2023, it fell dramatically to around 5.4 per cent by December 2025, easing pressure on households and businesses. This allowed the Bank of Ghana to lower its policy rate to 15.5 % in early 2026, while still keeping an eye on inflation. The economy remained resilient, growing about 5.7 per cent in 2024 and maintaining quarterly growth above 5 % through late 2025, thanks to strong performance in sectors like services, agriculture, and exports. Ghana’s current account surplus and reserves, equal to about 5–6 months of imports, also helped stabilise the Cedi and build investor confidence. Even with these improvements, global uncertainties continue to shape local financing.

High bond yields and cautious investors mean banks remain selective about lending, keeping borrowing costs high for businesses and households. On the fiscal side, better revenue collection and successful debt restructuring, along with support from the IMF Extended Credit Facility, have helped narrow the budget deficit and maintain confidence in the country’s economic stability. In short, Ghana’s economy is navigating a delicate balance: external shocks like rising oil prices or geopolitical tensions can affect investments and borrowing costs, but sound macroeconomic policies and growing reserves have helped cushion the impact, giving the private sector a more stable environment to grow.

Government budget and fiscal discipline

It is an undeniable fact that government budgets in Ghana have long been under strain from multiple pressures. Rising global energy prices increase the need for energy subsidies, while higher global interest rates push up debt service costs, eating into already limited fiscal resources. At the same time, slower economic growth reduces both tax and non-tax revenue, narrowing the space available for essential public services. According to the 2025 national budget, total government revenue (including grants) was projected at around GH₵224.9 billion, roughly 16–17 per cent of GDP, while total expenditure was set at about GH₵268–269 billion (around 19 per cent of GDP), resulting in a budget deficit of about 3–3.1 per cent of GDP that would need to be financed through borrowing. Of this revenue, roughly 34 per cent is absorbed by the public sector wage bill, which amounted to GH₵76.6 billion (5.5 per cent of GDP), while interest payments on public debt accounted for another GH₵64.2 billion (4.6 per cent of GDP). This sizable allocation limits flexibility for other priorities.

These pressures make fiscal consolidation, the effort to control deficits and manage debt, more difficult. On top of this, ongoing geopolitical tensions involving Iran, Israel, and the United States compound uncertainty. Escalated conflict can disrupt global energy and shipping markets, raising fuel and import costs for Ghana. Higher import bills weaken the Cedi, increase domestic inflationary pressures, and reduce real purchasing power, all of which can further depress tax receipts. Meanwhile, if investor confidence falters, borrowing costs could rise further, forcing even larger interest payments and squeezing funds available for public services and capital investments. The government’s wage bill is also vulnerable in such an environment. Rising costs of living can prompt public sector workers to seek higher compensation, and the government must continue to deliver essential services. With more than one-third of revenue already absorbed by wages, these pressures risk crowding out other critical areas, including health, education, and infrastructure.

Energy sector: Import dependence and cost pressures

Ghana remains a net importer of refined fuels despite increasing domestic crude production from offshore fields such as Jubilee and TEN. As a result, changes in global crude prices quickly translate into higher domestic fuel costs. For instance, during the January 2026 Brent crude spike above $95 per barrel, the landed cost of petrol and diesel in Ghana rose correspondingly. This has several significant implications. First, it increases government subsidy requirements, as the state often intervenes to stabilise pump prices, placing additional pressure on public finances. Second, higher fuel costs escalate transport and logistics expenses, with fuel accounting for 30–40 per cent of inland haulage costs. Third, utility tariffs rise because thermal electricity generation, which relies on imported fuel, becomes more expensive. Even a relatively modest 10 per cent sustained increase in crude prices, for example, from $80 to $88 per barrel, can add tens of millions of dollars annually to Ghana’s import bills, squeeze fiscal space, and feed into inflation, affecting both businesses and households.

Other sectors

Apart from the aforementioned sectors, there is a high likelihood of spillover effects across other key sectors of the economy, with real implications for growth, employment, and stability. Agriculture alone contributes around 20–21 per cent of Ghana’s GDP and remains a major driver of growth, having expanded by as much as 8.6 per cent in the third quarter of 2025, and employs a significant share of the workforce, especially in rural areas where livelihoods depend on crop and food production. Rising fuel and transport costs therefore increase the price of agricultural inputs like fertiliser and diesel, raise the cost of moving produce to markets, and can threaten food availability and domestic food prices, which can, in turn, erode household welfare and raise living costs.

Many manufacturing and industrial firms rely on imported raw materials and intermediate goods; with global commodity price volatility and a weaker Cedi, input costs rise significantly, squeezing margins and reducing competitiveness. In the industry sector, manufacturing and construction account for roughly 28–29 per cent of GDP, meaning that cost shocks from energy and imports directly affect nearly a third of economic output. Higher input and logistics costs also affect Ghana’s trade and external sector by widening the trade deficit and depleting foreign exchange reserves while diminishing export competitiveness.

Overall, the interconnected nature of Ghana’s economic structure means that global shocks do not only affect energy or transport, but also ripple through nearly every sector, amplifying fiscal pressures, slowing growth, and affecting livelihoods. Understanding these transmission channels with supporting data is crucial for designing targeted, sector-specific interventions to mitigate negative impacts and strengthen resilience across the economy.

These dynamics have direct implications for employment and household welfare. Rising production and transport costs may prompt firms to scale back operations or delay expansion, reducing jobs in both formal and informal sectors. Households, in turn, face higher living costs as energy, transport, and food prices rise. In the construction and infrastructure sector, increased fuel and material costs drive up project expenses and can cause delays in both public and private developments. Even sectors that are less directly energy-intensive, such as telecommunications and the digital economy, are affected through higher operational costs, which may constrain investment in network expansion and impact service affordability. Finally, tourism and hospitality, a key components of the services sector, may face rising travel and operational costs alongside currency volatility, which can reduce visitor numbers, lower occupancy rates, and diminish foreign exchange earnings.

Comprehensive policy recommendations for sustaining Ghana’s economic gains

Honourable Minister, the evidence presented above shows that geopolitical shocks, particularly sharp increases in global crude oil prices, disruptions to trade routes, financial volatility, and rising imported costs, can transmit rapidly across Ghana’s economy. To deepen resilience, enhance growth, and protect households, the government should adopt a multi-pronged strategy anchored in historical performance and calibrated to current economic realities. To this end, part II of my letter to your respected office will seek to suggest some immediate structural recommendations. Thank you.

The writer is Prof. John Kwaku Mensah Mawutor, University of Professional Studies, Accra

Department of Accounting

Accra, Ghana