Financial markets have turned quite optimistic since we last published the Global Financial Stability Report (GFSR) in October 2023.

Expectations for a global economic soft landing and continued progress on disinflation have created an environment for households and businesses to obtain financing at lower costs, notwithstanding still-high interest rates.

Investors may also be reassured by the fact that the banking turmoil from last year appears to have been contained. A soft landing after a significant rise of global inflation is unusual by historical standards.

Since the 1970s, meaningful tightening of monetary policy to reduce inflation has usually been followed by recessions and a tightening of financial conditions. This time around, markets seem to expect resilient, albeit low, growth in most countries as inflation returns to target.

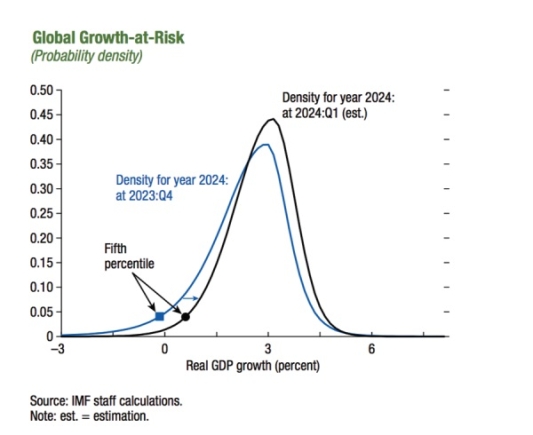

A soft landing is also the IMF’s baseline case, as documented by the April 2024 World Economic Outlook. But the job of the GFSR is to assess risks to global financial stability, which are inherently non-baseline possibilities.

So, while near-term downside risks may have receded since our October 2023 GFSR, there are still several salient risks at the top of our minds.

First, our models reveal stretched valuations in various asset classes, predominantly through compressed risk premiums relative to historical standards.

One example is the corporate bond market, where spreads continue to grind lower despite rising default rates. Another example is the sovereign debt market, where spreads, even for vulnerable issuers, have narrowed.

But stretched valuations aren’t limited to bonds—they’re also noticeable in stock and even some commodity markets. Prices of assets have moved up together, riding the wave of lower risk premiums, increasing asset price correlations, and lowering market volatility.

This is an environment in which asset repricing can happen quickly. Sudden shifts in policies, a flare-up of geopolitical tensions, and commodity and supply chain disruptions are a few examples of catalysts that could usurp current expectations of the trajectory of inflation and, in turn, monetary policy.

Financial conditions

Financial conditions would then tighten sharply as investor sentiment sours and asset price correlations decline. A less favorable financing environment, in turn, would likely exacerbate existing fragilities.

As detailed in this GFSR, borrowers in real estate markets, especially certain segments of commercial real estate with weak prospects, could face difficult and costly re financings of existing loans, like the estimated 600 billion of US commercial real estate debt that is due this year.

Defaults would then ensue, putting pressure on lenders with concentrated exposures in these loans. More broadly, default rates in riskier credit markets have been rising in many countries.

If global financial conditions were to tighten, capital outflow pressures on emerging markets could emerge, putting currencies and other assets under depreciation pressure.

That said, major emerging markets have weathered well through interest rate hikes over the past few years, demonstrating domestic resilience built with improved policy frameworks.

Weaker sovereigns, on the other hand, may once again see their international sources of funding dry up. In the medium term, easy financial conditions are conducive to the accumulation of financial vulnerabilities, such as the overuse of debt by both governments and private-sector borrowers.

For governments, concerns about debt sustainability could further intensify. In the private sector, the rapid surge in private credit over the past few years—lending by institutions that are not regulated like commercial banks or other traditional players—could expose fragilities given how opaque this market is.

Macro-financial stability

Another source of concern for macro-financial stability is the growing risk of malicious cyber-attacks associated with the deepening digitalization and reliance on technology.

Reassuringly, policymakers can take steps to mitigate these salient risks and reduce vulnerabilities. Such steps need to be taken decisively, starting with pushing back against overly optimistic expectations of the pace of disinflation and monetary policy easing.

By doing so, asset repricing risks could be mitigated. This has been the IMF’s advice for some time, and recent communications by major central banks cautioning that disinflation has not yet been fully achieved are consistent with this recommendation.

Financial regulatory authorities should take steps to ensure banks and other institutions can withstand defaults and other risks, using stress tests, early corrective actions, and other supervisory tools.

Where there are data gaps, like in private credit markets, reporting requirements should be enhanced. Regulators should prioritize full and consistent implementation of internationally agreed prudential standards, notably finalizing the phase-in of Basel III.

Further progress on recovery and resolution frameworks is also of first-order importance, to limit the fallout from the demise of weaker institutions.

Debt vulnerabilities

Authorities should strengthen efforts to contain debt vulnerabilities, including through appropriate fiscal consolidation, as recommended by the April 2024 Fiscal

Monitor.

For emerging markets and frontier economies, such efforts should lessen the incidence and severity of capital outflows and external funding squeezes.

The overall outlook for global macro-financial stability risks has improved in the past year, alongside declines in global inflation. However, policymakers must remain vigilant and plan for action not just in the baseline but also in adverse scenarios.

Since the outbreak of the COVID-19 pandemic in 2020, financial sectors and economies have been hit by a series of adverse shocks, and further downsides could materialize. Only prudent policy and alert readiness will ensure that potential future scenarios can be tackled effectively.