Cedi debate, needless, dishonest and deliberate misinformation

The debate around the depreciating cedi has resurfaced. BoG, whose duty it is to independently and sacredly manage the performance of the cedi against its trading partners has somewhat been politicised.

For instance, if the BoG at a point is suffering from depressed reserves, leading to liquidity challenges, and the market is unaware, speculative or panic behaviour may be absent. However, if the market is aware because the BoG’s management of the currency has been exposed through a Dr Bawumia-induced scrutiny, the country would have been revealing the challenge over a period to market participants.

The result will be an uptick in speculative behaviour to the detriment of the currency. Once this is made a cycle, it becomes difficult to manage.

Therefore, politicising currency management is the worse that should ever happen; it deepens the scrutiny of BoG’s currency management role in a way that creates further fear and panic, especially when the information from the central bank does not give comfort. Sadly, that information is neither what the government nor the BoG say but what is available to analysts and market participants.

Closely related to that is the fact that Ghana needs a stable currency, not a strong one, as Dr Bawumia would have us believe.

As a lower middle-income country, Ghana needs to import less and export more. To do that we need to maintain a fairly stable, not strong currency to make our exports cheaper abroad, similar to what makes Chinese exports a toast of the world.

So ‘strong currency’ goes against the government’s ‘One District, One Factory’ agenda.

While I do not expect BoG’s Governor, Dr Ernest Addison, to openly rebuke the vice president, given Dr Addison’s depth on the matter, I expect that he smartly points Dr Bawumia to the dangers and disservice his continuous, inaccurate and needless politicisation of currency management is bringing to the nation and the BoG in particular.

Worsening cedi

A review of data from BoG

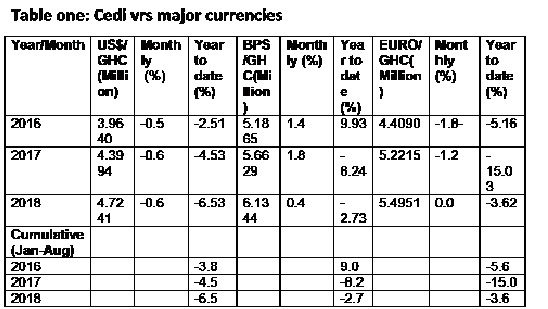

Let us look at the year-on-year performance of the cedi in August 2016 to 2018 as well as the cumulative performance for

It is clear from the exchange rates, cedi depreciation and appreciation data in table one that the cedi has depreciated significantly against the major trading currencies in cumulative terms, from January to August 2018.

While the cedi experienced marginal year-to-date depreciation of 2.51 per cent against the US dollar in August 2016, it experienced a higher depreciation of 4.53 per cent in the same period in 2017.

The 2016 depreciation, however, more than doubled to an alarming rate of 6.53 per cent in August 2018.

The cumulative analysis of the depreciation of the cedi against the dollar from January to August shows a consistently worsening cedi, with a depreciation from 3.8 per cent in 2016 to 4.5 per cent in 2017 and 6.5 per cent in 2018.

In terms of the pounds sterling, the cedi deteriorated from a stronger position in 2016, when it appreciated by nine per cent to depreciate at 8.24 per cent in 2017 and 2.7 per cent in 2018.

Although the cedi has recovered from its collapse against the pound, it is still worse off than the strong performance in 2016. Yet, Dr Bawumia says the cedi is in the best it has ever been.

Against the euro, the cedi depreciated by over 15 per cent in the same period in 2017 compared to a depreciation of 5.16 in the same period in 2016.

Although it has improved in 2018, it is a herculean task for it to recover the 15 per cent per cent depreciation experienced in 2017. Yet again, Dr Bawumia says the cedi is in top form.

Warped logic

While it is generally expected that increased rates in a country may lead to

With the cedi losing value to the euro, pound and even the CFA in Francophone West Africa, the question to ask

Did the European Union also increase interest rates to cause the cedi to depreciate by 15 per cent against the euro?

Did the British increase interest rates to cause the cedi to move from a strong position of nine per cent appreciation in 2016 to a depreciation of 8.24 per cent in 2017 and 2.7 per cent in 2018?

It is obvious that the cedi’s woes are more than interest rate hikes in America. Needless to

Are all these caused by interest rate hikes in those countries?

Real

A review of BoG data shows that the cedi is suffering from

The cedi has been badly exposed by lack of appropriate cover for imports, unsustainable borrowing by the central bank to support the cedi and the general slowdown of the real sector of the economy, leaving the minerals and oil and gas subsectors to shoulder the task of forex inflows and liquidity in the market.

Of critical importance are;

1. Worsening net international reserves and import cover

The country’s trade balance began to see improvement towards the fourth quarter of 2016. This resulted from upscale of oil and gas output from the Jubilee Fields after the turret bearing problem of the FPSO that had affected production negatively in the first half of 2016 had been resolved.

By the end of 2016, Ghana was beginning to become a net exporter of oil and gas. As a result, we significantly relied on our own gas from Atuabo to power our thermal plants, thereby reducing significantly our importation of gas and light crude. This positively impacted our trade balance.

By 2017, we strongly improved our production of crude and gas at the start of production from the TEN and Sankofa Gye-Nyame fields, which made us

The writer is

Bolgatanga Central

Email: