Underage drivers and motor insurance

IT is an indisputable fact that many people still have issues with comprehensive motor insurance. Many are of the view that once a vehicle is comprehensively insured, it means claims must be paid regardless of whatever happens to that vehicle or its occupants or third parties at any given time.

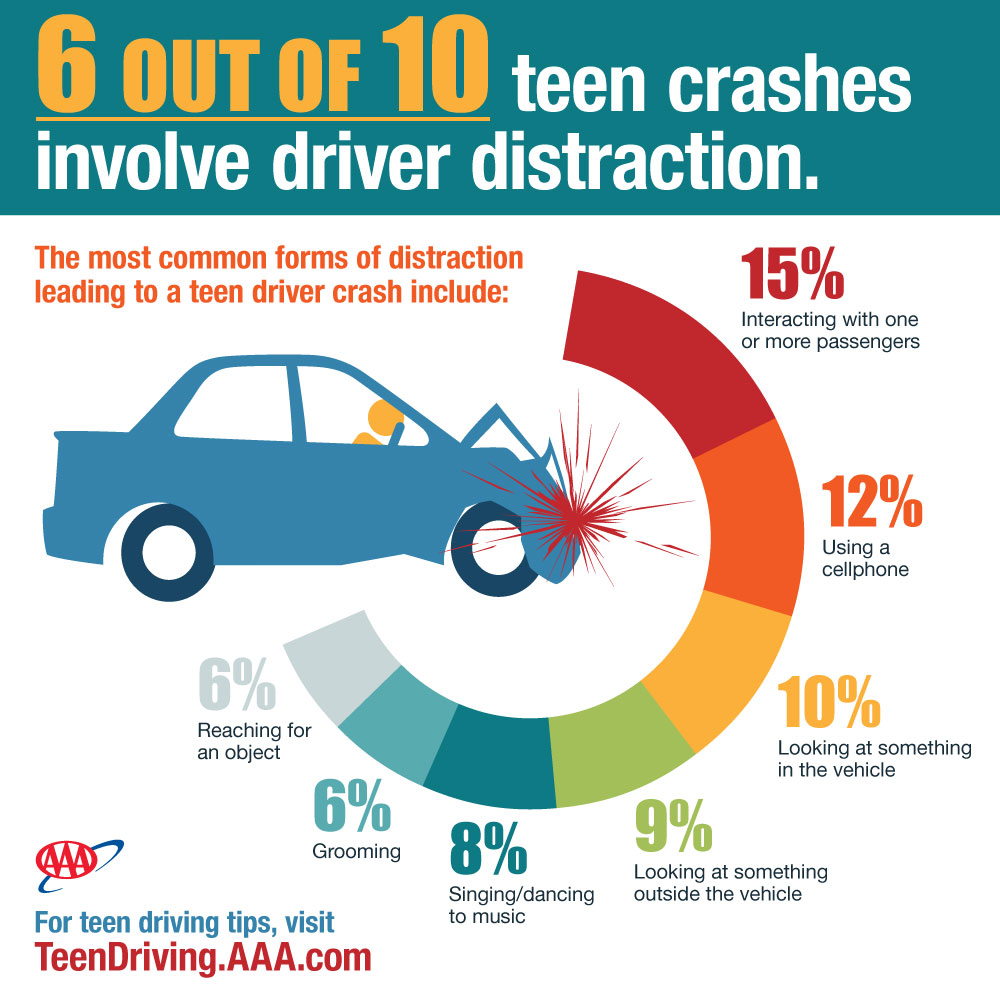

Teenagers on the road

There is a growing trend in the way some parents consciously or otherwise permit their underage children to drive their vehicles.

A parent parks her vehicle in the garage, asks her teenage child (14-17) to wash it. Adventurous as the case has mostly been, these teenagers learn to move the vehicles on their own, drive them out often at the blind side of their parents and then the ‘expected’ happens - crash!

I often meet people who still assume that anybody can drive their vehicles once it is comprehensively insured. It is worthy to note that technically, it is not the vehicle that is insured but the person driving it! Confusing, I guess but this only plays out in the event of a claim!

The following scenario would serve as case studies to highlight some of the events comprehensive motor insurance will ‘frown at’. Though these exclusions are often applied, they are done so much to the chagrin of some policyholders.

Scenario

Mr Abeka whose family lives in Accra works in Cape Coast. He visits his family once every two weeks. His wife doesn’t drive. He has a 14-year old JHS son, Ebo. In his garage are two saloon cars. His wife, Mrs Abeka, hardly drives and would not touch any of the vehicles even if it becomes really necessary. Ebo washes the two cars at least once every week. Mrs Abeka sends Ebo on an errand last Saturday and he is to go in a taxi.

Ebo, in the bid to show off his parents’ wealth in addition to his own driving skills, stealthily drives one of the vehicles and succeeds in making at least 8km into the errand and back.

His mother seems to have ‘encouraged’ Ebo based on the fact that her son is capable of driving a car!

Schools on recess

Schools go on recess and it is time for students to show off how wealthy their parents are. Ebo, whose confidence level had inched up from his previous ‘successful’ trip, sneaks out with the second car with the mother, not really concerned about his own safety!

This time round, he isn’t lucky. He runs into two young siblings killing one instantly and maiming the other severely!

Driving without licence

In insurance and in common law, it can be impugned that a driver of a vehicle without a valid driving licence is a moral hazard and more likely to cause an accident than one with a licence, all things being equal. In our typical traditional setting, the devil would be compelled to accept the blame here!

Technically, the proximate cause of the accident remained largely inexperience and technical incompetence. Allowing an underage and unlicenced child to drive a vehicle might be a criminal offence and the law would not let go on this one.

Insurance claims

It is clear from the above picture that following the accident, a claim ‘should’ be made, after all, the vehicle was comprehensively insured!

The fact that he was a minor without a licence, making an insurance claim would be difficult!

Can insurance be blamed?

Motor insurance is insurance purchased for cars, trucks, and other road vehicles with its primary objective being to provide protection against physical damage resulting from traffic collisions and against liabilities that could also arise therefrom.

However, it is worth noting that motor insurance just like any other form of insurance also has exclusions.

The things not covered

The following are some of the most important things the insured needs to know about especially comprehensive insurance in relation to this scenario.

- Any accident, injury, loss or damage while any vehicle that is insured under this policy is being driven by or is in the charge of any person for the purposes of being driven who:

is not described under the section of your certificate of motor insurance headed "Permitted drivers" (P), or

does not have a valid and current licence to drive your vehicle, or

is not complying with the terms and conditions of the licence, or does not have the appropriate licence for the type of vehicle. For example, a licence B driver is not permitted to drive a 4 x 4 vehicle!

Insurance will not pay for any accident, injury, loss or damage while any vehicle that is insured under this policy is being used other than for the purposes described under the "Description of use" section of the Motor Insurance Certificate, or an auto insurance exclusion which is clearly stated in the policy document.

- Loss or destruction of, or damage to, any property or associated loss or expense, or any other loss.

Indeed insurance laws mandate which exclusions can be offered to drivers. Generally, auto insurance exclusion types that are available for consumers to write into their policy include the following available options:

Options available

1. Driver Exclusions: This exclusion states that a specific person who has access to your motor vehicle is not covered under your car insurance policy.

2. Bodily Injury: Some insurance companies will not cover you for compensation if you are involved in an auto accident while using your car or truck to carry passengers or materials. (This is the reason many Ghanaian motorists especially those who have sojourned in the western world are accused of ‘not offering people lift because they are wicked’).

3. Employees: If you are a business owner you might have an exclusion written into your car insurance policy that states the insurance company will not reimburse you for damage made to an employee who operates your motor vehicle.

Advice to members of the motor insuring public

Auto insurance accidents that you cause on purpose are generally considered to be exclusions. Make sure that you read through your car insurance policy thoroughly. This will help you to understand the exclusions that apply to your coverage.

If you are purchasing a motor insurance, ask the insurance officers or agents to tell you about general exclusions that the company writes in policies. Also ask the officer or agent about additional exclusions that you can request the insurance company to write into your particular policy.

From the scenario above, we must note that a minor is a minor and must not drive a car until they reach the statutory age required to qualify for a valid licence.

For that matter, this is an exclusion that cannot be bought back as is the case with buying other excesses! This must be a guiding principle to parents as we welcome our children back from school!