Banks rethink income strategy • As T-Bill yield falls to 6.45%

The yield on the 91-day Treasury bill has dropped sharply to 6.45 per cent, raising concerns among fixed income investors and pushing banks to rethink how they generate revenue as returns from government securities continue to decline.

The rapid fall in Treasury bill yields meant banks and investors would need to adjust their strategies, particularly as many financial institutions depended heavily on returns from government instruments.

The development has also sparked debate among market watchers about the implications for pension funds, banks and investors, as the fixed income market experiences one of the steepest yield declines in recent years.

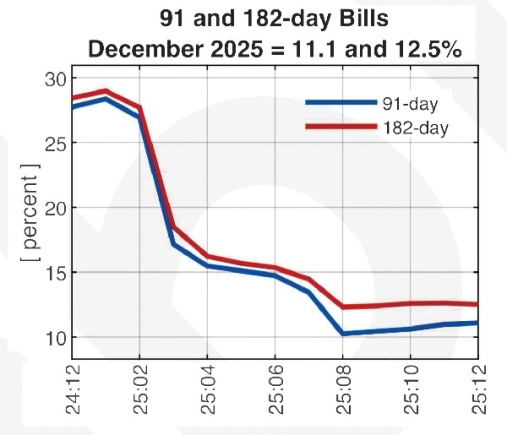

The 91-day Treasury bill yield fell from 8.6095 per cent last week to 6.45 per cent, continuing a steady downward trend in government borrowing costs.

Earlier this year, the short-term instrument has dropped to 11.1165 per cent on January 5, 2026. It was as high as 28.0363 per cent in December 2024

Chief Executive Officer (CEO) of Millennium Development Authority , Alex Mould, said the sharp decline would significantly affect investors who relied on fixed income securities for stable returns, particularly pension funds and pensioners.

“Investors who depend on treasury instruments would see their income fall sharply because the yields had dropped to levels that were far lower than what they enjoyed in previous years,” he said.

Mr Mould said the decline in yields would also affect the banking sector because many banks invested a large portion of their deposits in government Treasury bills.

He explained that in many cases, banks invested more than 50 per cent of their deposits in government securities, meaning the drop in yields would reduce their net interest income.

“Banks had depended heavily on treasury investments, so once the yields have started falling their earnings from interest income would also decline,” he said.

Mr Mould added that bank stocks on the Ghana Stock Exchange might not perform strongly this year compared with 2025 because of the reduced income from Treasury bill investments.

Search for new income

He said banks were already looking for alternative revenue streams to offset the decline in interest income from government securities.

“Banks were examining other areas of income because the fall in Treasury bill yields meant their traditional earnings model was under pressure,” he said.

Analysts say some would attempt to increase fees and charges to compensate for declining returns from treasury investments.

But Mr Mould cautioned customers and regulators to resist excessive fee increases to prevent further pressure on consumers.

“Banks could try to raise fees, but regulators and customers would have to ensure that such increases did not place unnecessary burden on the public,” he said.

Mr Mould said the fall in yields would push banks to increase lending to consumers, businesses and industries as a way to maintain profitability.

He explained that banks that managed credit carefully would remain profitable, while those that failed to manage lending risks could face rising non-performing loans.

“Banks that practised disciplined lending would continue to make profits, but those that extended credit without proper risk assessment would eventually face higher bad loans,” he said.

He therefore advised investors to carefully assess where they placed their funds as the market environment continued to change.

Monetary policy outlook

Attention is now turning to the upcoming monetary policy meeting of the Bank of Ghana scheduled for March 16 to March 18.

Market analysts expect the central bank to reduce the Monetary Policy Rate, currently above 15 per cent, by about 2.5 percentage points to around 13 per cent.

Mr Mould said a reduction in the policy rate would further lower borrowing costs and provide the government with more fiscal space to finance key programmes.

“Lower interest payments on debt servicing would give the government more room to spend on important policy initiatives,” he said.

He also indicated that the government might soon test the domestic bond market for longer-term financing.

According to him, the authorities could issue bonds with maturities of five to 10 years once interest rates stabilised at lower levels.

Mr Mould said the government could target yields of around 10 per cent for five-year bonds, 11 per cent for seven-year bonds and about 12 per cent for ten-year bonds.

“In the coming months government would likely enter the bond market to determine investor appetite for longer-term securities at lower rates,” he said.

Market implications

Despite the fall in treasury yields, the 364-day Treasury bill continues to trade around 12 to 13 per cent, although authorities expect this to decline to single-digit levels over time.

Mr Mould said if inflation did not fall significantly, investors could experience negative real returns, which might push them to seek alternative investments such as gold or foreign currencies as a hedge against currency depreciation.

He added that the shift away from fixed-income securities could also drive more investors toward equities on the Ghana Stock Exchange. “Funds that were previously invested in treasury bills could move into the stock market, although some investors might buy shares based on sentiment rather than company performance,” he said.

The decline in Treasury bill rates follows a broader effort by the government and the central bank to reduce borrowing costs after the country’s debt restructuring and stabilisation programme supported by the International Monetary Fund (IMF).