Moderating inflation and steady growth open path to soft landing (2)

In emerging market and developing economies, growth is expected to remain at 4.1 percent in 2024 and to rise to 4.2 percent in 2025.

An upward revision of 0.1 percentage point for 2024 since October 2023 reflects upgrades for several regions.

• Growth in emerging and developing Asia is expected to decline from an estimated 5.4 percent in 2023 to 5.2 percent in 2024 and 4.8 percent in 2025, with an upgrade of 0.4 percentage point for 2024 over the October 2023 projections, attributable to China’s economy.

Growth in China is projected at 4.6 percent in 2024 and 4.1 percent in 2025, with an upward revision of 0.4 percentage point for 2024 since the October 2023 WEO.

The upgrade reflects carryover from stronger-than- expected growth in 2023 and increased government spending on capacity building against natural disasters.

Growth in India is projected to remain strong at 6.5 percent in both 2024 and 2025, with an upgrade from October of 0.2 percentage point for both years, reflecting resilience in domestic demand.

• Growth in emerging and developing Europe is projected to pick up from an estimated 2.7 percent in 2023 to 2.8 percent in 2024, before declining to 2.5 percent in 2025. The forecast upgrade for 2024 of 0.6 percentage point over October 2023 projections is attributable to Russia’s economy.

Growth in Russia is projected at 2.6 percent in 2024 and 1.1 percent in 2025, with an upward revision of 1.5 percentage points over the October 2023 figure for 2024, reflecting carryover from stronger-than-expected growth in 2023 on account of high military spending and private consumption, supported by wage growth in a tight labor market.

• In Latin America and the Caribbean, growth is projected to decline from an estimated 2.5 percent in 2023 to 1.9 percent in 2024 before rising to 2.5 percent in 2025, with a downward revision for 2024 of 0.4 percentage point compared with the October 2023 WEO projection.

The forecast revision for 2024 reflects negative growth in Argentina in the context of a significant policy adjustment to restore macroeconomic stability.

Among other major economies in the region, there are upgrades of 0.2 percentage point for Brazil and 0.6 percentage point for Mexico, largely due to carryover effects from stronger-than-expected domestic demand and higher-than-expected growth in large trading-partner economies in 2023.

• Growth in the Middle East and Central Asia is projected to rise from an estimated 2.0 percent in 2023 to 2.9 percent in 2024 and 4.2 percent in 2025, with a downward revision of 0.5 percentage point for 2024 and an upward revision of 0.3 percentage point for 2025 from the October 2023 projections.

The revisions are mainly attributable to Saudi Arabia and reflect temporarily lower oil production in 2024, including from unilateral cuts and cuts in line with an agreement through OPEC+ (the Organization of the Petroleum Exporting Countries, including Russia and other non- OPEC oil exporters), whereas non-oil growth is expected to remain robust.

• In sub-Saharan Africa, growth is projected to rise from an estimated 3.3 percent in 2023 to 3.8 percent in 2024 and 4.1 percent in 2025, as the negative effects of earlier weather shocks subside and supply issues gradually improve.

The downward revision for 2024 of 0.2 percentage point from October 2023 mainly reflects a weaker projection for South Africa on account of increasing logistical constraints, including those in the transportation sector, on economic activity.

Inflation Outlook:

Steady Decline to Target Global headline inflation is expected to fall from an estimated 6.8 percent in 2023 (annual average) to 5.8 percent in 2024 and 4.4 percent in 2025.

The global forecast is unrevised for 2024 compared with October 2023 projections and revised down by 0.2 percentage point for 2025.

Advanced economies are expected to see faster disinflation, with inflation falling by 2.0 percentage points in 2024 to 2.6 percent, than are emerging market and developing economies, where inflation is projected to decline by just 0.3 percentage point to 8.1 percent.

The forecast is revised down for both 2024 and 2025 for advanced economies, while it is revised up for 2024 for emerging market and developing economies, mainly on account of Argentina where the realignment of relative prices and elimination of legacy price controls, past currency depreciation, and the related pass-through into prices is expected to increase inflation in the near term.

The drivers of declining inflation differ by country but generally reflect lower core inflation as a result of still-tight monetary policies, a related softening in labor markets, and pass-through effects from earlier and ongoing declines in relative energy prices.

Overall, about 80 percent of the world’s economies are expected to see lower annual average headline and core inflation in 2024.

Among economies with an inflation target, headline inflation is projected to be 0.6 percentage point above target for the median economy by the fourth quarter of 2024, down from an estimated gap of 1.7 percentage points at the end of 2023.

Most of these economies are expected to reach their targets (or target range midpoints) by 2025. In several major economies, the downward revision to the projected path of inflation, combined with a modest upgrade to economic activity, implies a softer-than-expected landing.

Risks to the outlook

With the likelihood of a hard landing receding as adverse supply shocks unwind, risks to the global outlook are broadly balanced. There is scope for further upside surprises to global growth, although other potential factors pull the distribution of risks in the opposite direction.

Upside risks. Stronger global growth than expected could arise from several sources:

• Faster disinflation: In the near term, the risk that inflation will fall faster than expected could again become a reality, with stronger-than-expected pass-through from lower fuel prices, further downward shifts in the ratio of vacancies to unemployed persons, and a compression of profit margins to absorb past cost increases.

Combined with a decline in inflation expectations, such developments could allow central banks to move forward with their policy-easing plans and could also contribute to improving business, consumer, and financial market sentiment, as well as raising growth.

• Slower-than-assumed withdrawal of fiscal support: Governments in major economies might withdraw fiscal policy support more slowly than necessary and than assumed during 2024–25, implying higher-than-projected global growth in the near term.

However, such delays could in some cases exacerbate inflation and, with elevated public debt, result in higher borrowing costs and a more disruptive policy adjustment, with a negative impact on global growth later on.

• Faster economic recovery in China: Additional property sector–related reforms––including faster restructuring of insolvent property developers while protecting home buyers’ interests––or larger- than-expected fiscal support could boost consumer confidence, bolster private demand, and generate positive cross-border growth spillovers.

• Artificial intelligence and supply-side reforms: Over the medium term, artificial intelligence could boost workers’ productivity and incomes, although this would depend on countries’ harnessing the potential of artificial intelligence.

Advanced economies may experience benefits from artificial intelligence sooner than emerging market and developing economies, largely because their employment structures are more focused on cognitive-intensive roles.

For emerging market and developing economies with constrained policy environments, faster progress on implementing supply-enhancing reforms could result in greater-than-expected domestic and foreign investment and productivity and faster convergence to higher income levels.

Downside risks. Several adverse risks to global growth remain plausible

• Commodity price spikes amid geopolitical and weather shocks: The conflict in Gaza and Israel could escalate further into the wider region, which produces about 35 percent of the world’s oil exports and 14 percent of its gas exports.

Continued attacks in the Red Sea––through which 11 percent of global trade flows––and the ongoing war in Ukraine risk generating fresh adverse supply shocks to the global recovery, with spikes in food, energy, and transportation costs.

Container shipping costs have already sharply increased, and the situation in the Middle East remains volatile. Further geoeconomic fragmentation could also constrain the cross-border flow of commodities, causing additional price volatility.

More extreme weather shocks, including floods and drought, could, together with the El Niño phenomenon, also cause food price spikes, exacerbate food insecurity, and jeopardize the global disinflation process.

• Persistence of core inflation, requiring a tighter monetary policy stance: A slower-than-expected decline in core inflation in major economies due, for example, to persistent labor market tightness and renewed tensions in supply chains could trigger a rise in interest rate expectations and a fall in asset prices, as in early 2023.

Such developments could increase financial stability risks, tighten global financial conditions, trigger flight-to-safety capital flows, and strengthen the US dollar, with adverse consequences for trade and growth.

• Faltering of growth in China: Absent a comprehensive restructuring policy package for the troubled property sector, real estate investment could drop more than expected, and for longer, with negative implications for domestic growth and trading partners.

Unintended fiscal tightening in response to local government financing constraints is also possible, as is reduced household consumption in a context of subdued confidence.

• Disruptive turn to fiscal consolidation: Fiscal consolidation is necessary in many economies to deal with rising debt ratios. But an excessively sharp shift to tax hikes and spending cuts, beyond what is envisaged, could result in slower-than-expected growth in the near term.

Adverse market reactions could pressure some countries that lack a credible medium-term consolidation plan or face a risk of debt distress to undertake harsh adjustments. In low-income countries and emerging market economies, the risk of debt distress remains elevated, constraining scope for necessary growth-enhancing investments.

Policy priorities

As inflation declines toward target levels across regions, the near-term priority for central banks is to deliver a smooth landing, neither lowering rates prematurely nor delaying such lowering too much.

With inflation drivers and dynamics differing across economies, policy needs for ensuring price stability are increasingly differentiated. At the same time, in many cases, amid rising debt and limited budgetary room to maneuver, and with inflation declining and economies better able to absorb effects of fiscal tightening, a renewed focus on fiscal consolidation is needed.

Intensifying supply- enhancing reforms would facilitate both inflation and debt reduction and enable a durable rise in living standards.

Managing the final descent of inflation. The faster-than-expected fall in inflation is allowing an increasing number of central banks to move from raising policy rates to adjusting to a less restrictive stance.

In this context, ensuring that wage and price pressures are clearly dissipating and avoiding the appearance of prematurely “declaring victory” will guard against later having to backpedal in the event of upside surprises to inflation.

At the same time, where measures of underlying inflation and expectations are clearly moving toward target-consistent levels, adjusting rates to more neutral levels––while signaling continued commitment to price stability––may be necessary (considering long transmission lags) to avoid protracted economic weakness and target undershoots.

In some emerging market economies, in which the monetary tightening cycle paved the way for earlier rate reductions, continuing to calibrate the pace of monetary adjustments based on a broad array of wage and price pressure gauges is appropriate.

With borrowing costs still high, careful monitoring of financing conditions and readiness to deploy financial stability tools will remain vital for avoiding financial sector strains.

Rebuilding buffers to prepare for future shocks and achieving debt sustainability. With fiscal deficits above prepandemic levels and higher debt-service costs, fiscal consolidation based on credible medium-term plans, with the pace of adjustment depending upon country-specific circumstances, is warranted to restore room for budgetary maneuver. Increasing fiscal balances over a sustained period, while protecting priority investments and support to the vulnerable, is needed in many cases.

Well-calibrated plans can support fiscal policy credibility, allow the pace of consolidation to be adjusted as a function of the strength of private demand, and avert disruptive front-loaded adjustments. Mobilizing domestic revenue, addressing spending rigidities, and reinforcing institutional fiscal frameworks are likely to support adjustment efforts, both in economies with sizable spending needs and in others as well.

For countries in or at high risk of debt distress, orderly debt restructuring may also be necessary. Faster and more efficient coordination on debt resolution, through the Group of Twenty Common Framework and the Global Sovereign Debt Roundtable, would help mitigate the risk of debt distress spreading.

Enabling durable medium-term growth. Targeted and carefully sequenced structural reforms can reinforce productivity growth and reverse declining medium-term growth prospects despite constrained policy space.

Bundling reforms that alleviate the most binding constraints to economic activity can front-load the resulting output gains, even in the short term, and secure public buy-in.

Industrial policies can be pursued where clearly identifiable externalities or important market failures are well established and other more effective policy options are unavailable, but the policies need to be consistent with World Trade Organisation (WTO) rules.

Such policies are more likely to be successful if complemented with appropriate economy-wide reforms and good governance frameworks. Carbon pricing, subsidies for green investments, reducing energy subsidies, and carbon border-adjustment mechanisms can speed the green transition but must be designed to support consistency with WTO rules.

Investments in climate adaptation activities and infrastructure are also needed to support resilience.

Strengthening resilience through multilateral cooperation. Intensified cooperation in areas of common interest is vital for mitigating the costs of the separation of the world economy into blocs.

In addition to coordination on debt resolution, cooperation is required to mitigate the effects of climate change and facilitate the green energy transition, building on recent agreements at the 2023 Conference of the Parties to the UN Framework Convention on Climate Change (COP28).

Safeguarding the transportation of critical minerals, restoring the WTO’s ability to settle trade disputes, and ensuring the responsible use of potentially disruptive new technologies such as artificial intelligence by, among other things, upgrading domestic regulatory frameworks and harmonizing global principles are further priorities.

The IMF Board of Governors’ conclusion of the 16th Review of Quotas is a welcome step that needs now to be followed by members’ providing their consent to their respective quota increases.

Global Financial Stability update

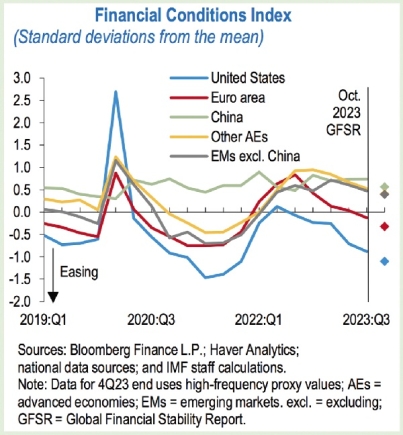

Since the October 2023 Global Financial Stability Report, inflationary pressures have continued to recede, fueling expectations that monetary policy in advanced economies will ease in the coming quarters.

The resulting momentous decline in interest rate expectations in December has driven a broad-based rally in risky assets. Global financial conditions have loosened, on net, since October, with that loosening driven by higher equity valuations, lower volatility, and already compressed corporate bond spreads.

Global bond yields have fallen significantly on net since October, especially at longer maturities. Real rates have driven declines throughout the curve, reflecting the market’s reassessment of the future interest rate environment.

For example, in the United States, after rising to levels last seen before the global financial crisis, 10-year real rates have reversed their trend to below 2 percent. Yields have increased since the beginning of 2024 as investors pare back expectations on the magnitude and pace of monetary policy easing by major central banks.

Investor optimism about the macro outlook stands in contrast to the deterioration of credit quality among borrowers.

Bank credit growth has fallen as the higher interest rates during 2023 have weighed on demand for loans while banks continue to exhibit lower risk tolerance.

In the meantime, defaults continue to mount for some segments of borrowers. Central banks’ balance sheet reduction so far has been orderly.

However, there are signs that lower liquidity in the financial system is starting to weigh on market functioning, particularly in certain short-term funding markets, with US repo funding rates having episodically spiked over the past few months.

Exposure of the banking system to commercial real estate is still a concern as tepid demand in some economies and higher borrowing costs increase risks of default among commercial real estate borrowers.

The recent insolvency of a giant European property company serves as a reminder of the fragilities the real estate sector faces in the current environment of volatile interest rates and falling real estate prices.

US banks also contend with still-sizable unrealized losses on available-for-sale and held-to-maturity securities. Despite the end-of-year rebound in equity markets, price-to-book ratios for US regional banks have not yet fully recovered from the March 2023 turmoil.

Amid significant interest rate volatility, the correlation between emerging market assets and US Treasury yields has increased. Higher yields in advanced economies have led to outflows in emerging market assets, although this has reversed since November for local currency assets.

Nevertheless, financial conditions in this higher-rate environment may continue to challenge economies in some regions, especially those of weaker emerging markets and countries with rapidly narrowing differentials against interest rates in the United States.