Understanding elements of ESG for effective sustainability reporting, disclosure

Environmental, Social and Governance (ESG) reporting has become topical in recent times such that corporate entities are gradually adapting their reporting systems and requirements to accommodate ESG.

Generally, sustainability reporting, which must have elements of ESG issues, is not new and has been in existence for some decades now, but the emphasis in recent times has a wider coverage and acceptability than in the past.

Several voluntary reporting frameworks have been developed in the past for sustainability reporting, some of which are still present in recent times.

The Global Reporting Initiative (GRI) founded in the late 90s, over the years, issued Sustainability Reporting Guidelines to guide entities to report performance indicators so that users can monitor their performance from economic, environmental and social perspectives.

The current sustainability reporting guidelines of GRI has a modular structure consisting of foundation, general disclosures and specific sustainability topics such as economic, environmental and social topics.

The contributions of bodies and organisations such as the International Integrated Reporting Council (IIRC), the Sustainability Accounting Standards Board (SASB), the Value Reporting Foundation (VRF) and the Task Force on Climate-Related Financial Disclosures to sustainability reporting and disclosure cannot be overemphasised.

The International Sustainability Standards Board (ISSB) was formed by the IFRS Foundation in 2021 with the objective of developing a global baseline of sustainability disclosure standards to complement IFRS Accounting Standards. The two IFRS Sustainability Disclosure Standards which were currently issued in June 2023 with effective date of 1st January 2024 are:

• IFRS S1 General Requirements for Disclosure of Sustainability-related Financial Information

• IFRS S2 Climate-related Disclosures

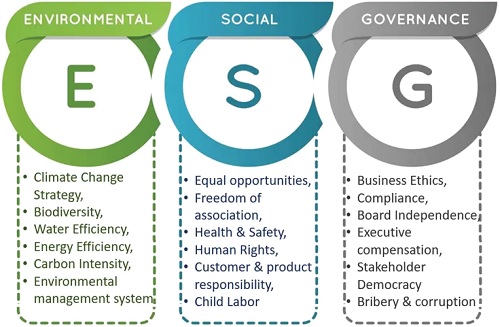

In this paper, the writers seek to explain briefly, the key content elements that must be disclosed under Environment, Social and Governance as part of sustainability reporting and disclosure.

Environment

• Materials used in an organisation’s operations and their impact on the environment. Key disclosures include: total weight or volume of materials used in operations; percentage of recycled materials used, distinguishing between internal and external sources; reuse and recyclability of products and packaging materials.

• Energy consumption and conservation. Key disclosures include: total energy consumption, including fuel consumption and electricity usage; energy intensity, which can be measured per unit of production or revenue; reductions in energy consumption by way of energy savings achieved through efficiency measures and initiatives.

• Water and effluents. Key disclosures include: total water withdrawal from various sources, including surface water, groundwater and third-party water; water discharge, including the volume and quality of effluent water; total water consumption, including water lost through evaporation, incorporation into products, or other means.

• Biodiversity. Key disclosures include: operational sites located in or near protected areas of biodiversity value; significant impact of activities, products, and services on biodiversity; information about habitats protected or restored.

• Emissions. Key disclosures include: direct Green House Gas (GHG) emissions from sources owned or controlled by the organisation; indirect GHG emissions from the generation of purchased or acquired electricity, steam, heat, or cooling; other indirect GHG emissions, such as those from supply chain activities; report on GHG emissions intensity, which can be measured per unit of production or revenue.

• Waste. Key disclosures include: information about waste generation and significant waste-related impacts; waste management practices and policies; total waste generated, including hazardous and non-hazardous waste; waste diverted from disposal through recycling, reuse, or other means; waste directed to disposal, including landfilling or incineration.

• Environmental compliance and instances of non-compliance. Key disclosure is instances of non-compliance with environmental laws and regulations.

• Supplier environmental assessment. Key disclosures include: the percentage of new suppliers that were screened using environmental criteria; report on negative environmental impacts identified in the supply chain and actions taken to address them.

• Environmental grievance mechanism. A process for stakeholders to report and address environmental concerns or grievances related to an organisation’s activities. Key issues include: the mechanism should be easily accessible to stakeholders, including local communities, employees, and suppliers; the process should be transparent, with clear procedures for reporting, investigating, and resolving grievances; grievances should be addressed in a timely manner, with regular updates provided to stakeholders; the mechanism should hold the organisation accountable for its environmental impacts and ensure that corrective actions are taken.

Social

• Employment policies, practices and performance. Key disclosures include: the total number of, and rate of, new employee hires and employee turnover; benefits provided to full-time employees that are not provided to temporary or part-time employees; the percentages of employees who took, and are entitled to, parental leave.

• Labour/management relations. Disclosure on the minimum notice period for operational changes that affect employees.

• Occupational health and safety. Key disclosures include: information about the organisation’s occupational health and safety management system; processes for identifying hazards, assessing risks, and investigating incidents; information about occupational health services provided to employees; report on worker participation, consultation, and communication on occupational health and safety matters; information about worker training on occupational health and safety; report on initiatives to promote worker health; information about prevention and mitigation of occupational health and safety impacts in business relationships; report on the percentage of workers covered by an occupational health and safety management system; information about work-related injuries; report on work related ill health.

To be continued with other social and governance disclosures in the next write up.

Stephen Mensah Dzodzodzi (PhD, CA, Ch.EE, Ch.PE, CGMA) is a chartered petroleum economist, a tax and management consultant and CEO of Centre for Professional Studies, Ho.

email:

Charles Ekornunye Ansah is a member of Chartered Institute of Tax Law and Forensic Accountants – Ghana (CITLFAG), and an Employee of Ghana TVET Service.

email: